Property taxes in Florida: DeSantis puts them on the ballot on November 3, 2026. Mayor Levine Cava warns of up to $977M in Miami-Dade losses

The Florida Legislature approved, in special session June 1-2, 2026, a constitutional amendment that will put the phase-out of the property tax on homestead homes to a vote of the voters in November 2026. If the amendment gets the required 60 percent, approximately 60 percent of Florida homestead homeowners would pay zero in non-school property taxes by 2028, with estimated savings of up to $2,672 annually in some counties.

For Miami-Dade County, on the other hand, the revenue loss would range from $697 million to $925 million in the first two years, according to estimates by the county government and Property Appraiser Tomas Regalado.

The central debate that will go to the polls in November is

Do Florida’s local governments have a revenue problem or a spending problem?

The special session called by Governor Ron DeSantis approved the proposal whose official ballot title, according to the enrolled text of CS/HJR 1F, is: SAVE OUR HOMES FROM EXCESSIVE PROPERTY TAXES.

- The text that will go on the ballot is House Joint Resolution CS/HJR1F introduced by Representative Toby Overdorf (R-Palm City) before the Florida House of Representatives.

- Senate Joint Resolution CS/SJR2-F by Senator Bryan Avila (R-Hialeah), simultaneously introduced as a companion resolution in the Senate, was laid on table on June 2, 2026 when the Senate proceeded to vote directly on the House version.

- The package includes CS/SB 4-F as state implementing legislation.

- The amendment raises the homestead exemption from $50,000 to $150,000 effective January 1, 2027.

- and to $250,000 on January 1, 2028, with a mandate to the Legislature to design a path toward the complete elimination of property tax homestead.

- Additionally, it reduces the limit on the annual increase in assessed value of non-homestead properties from 10 percent to 5 percent and imposes a five-year waiting period for new residents to access the expanded exemption.

- The amendment does not affect school levies.

It goes on the November 3, 2026 ballot and requires ratification by 60 percent of voters.

Key findings in 3 points

- The direct benefit to the homestead homeowner is quantifiable: according to Governor DeSantis, the amendment would completely eliminate the non-school property tax for approximately 60 percent of Florida homestead homeowners by 2028. The official SaveOurHomesFL.com calculator allows each homeowner to view their specific savings by address; on a $350,000 homesteaded home in Broward, the projected savings is $2,672 annually.

- The amendment passed with transpartisan support: three Democratic senators – MackBernard, Daryl Rouson and Barbara Sharief –voted in favor, and the final votes were 30 to 9 in the Senate and 75 to 26 in the House of those present and voting that day.

- The fiscal impact for Miami-Dade County ranges from $697 million in the first two years according to Major Cava’s projection (op-ed Miami Herald May 2026) to $925 million according to Property Appraiser Tomas Regalado ‘s estimate over the same period.

- Statewide, the loss to local governments is estimated by the Legislature at $4.6 billion in 2027 and $8.4 billion in 2028.

- The underlying debate is not whether public services are necessary but whether local governments have a spending or revenue problem.

- The First Budget Hearing 09.04.2025 – Miami-Dade Board of County Commissioners First Budget Hearing

- At the Board of County Commissioners ‘ second budget hearing on September 18, 2025, Commissioner Roberto J. Gonzalez (D11) accused the administration of“utter lack of information and transparency” throughout the budget process, proposed reducing the county’s operating millage by 1.8 percent and charged that $21 million of the overall budget was going to the FIFA World Cup when it should be funded by tourism funds.

- Major Cava responded that the commissioner’s speech “demonstrates the lack of knowledge of the budget process” and that her commissioner “repeatedly declined those meetings or canceled them at the last minute to score political points.”

What happened

Governor Ron DeSantis called the special session of the Florida Legislature June 1-2, 2026 under the title Save Our Homes from Excessive Property Taxes.

On June 1, 2026 and June 2, 2026, the Senate Appropriations Committee processed and advanced the proposal with changes, including the elimination of a $5.5 million line item that the executive had included to promote the amendment through the SaveOurHomesFL.com government website.

The elimination of this item was a direct result of pressure from legislators who questioned the use of public funds for an active electoral campaign in favor of a specific amendment. Both chambers voted on the same day, June 2: 75 to 26 in the House and 30 to 9 in the Senate, according to the official CS/HJR 1-F record; the chambers have 120 representatives and 40 senators in total, respectively.

The legislative package establishes five components.

- First, increase of the general homestead exemption from $50,000 to $150,000 effective January 1, 2027.

- Second, additional increase to $250,000 effective January 1, 2028, with a mandate to the State Legislature to design the complete elimination of the property tax homestead on a subsequent schedule.

- Third, reduction of the annual assessed value increase limit for non-homestead properties from 10 percent to 5 percent.

- Fourth, a new constitutional restriction limiting the use of ad valorem taxes collected by counties and municipalities exclusively to seven categories: public safety, public education and schools, infrastructure, natural resource projects, municipal bonds and payment of existing debt, retirement benefits for local government employees, and operations of county officials and municipalities under Article VIII.

- Fifth, a five-year waiting period for new Florida residents to access the expanded $250,000 exemption. The amendment does not affect school district levies, pursuant to Florida Constitution Article VII Section 4.

By requiring modification to the text of Florida Constitution Article VII Sections 4, 6 and 9 – and the creation of a new section in Article XII – the amendment must be ratified on the ballot. Under Florida Constitution Article XI Section 5, it requires 60 percent of the voters at the November 3, 2026 general election.

The clause that redefines local spending: what counties will be able to use the property tax for

The legislative package includes an element that has received less attention in state coverage than the homestead exemption but could have more permanent consequences on the fiscal autonomy of local governments:

the new Section 9(2) of the Florida Constitution, introduced by CS/HJR 1F if ratified by the voters in November. The section provides that ad valorem taxes collected by counties and municipalities shall be used only for seven taxable categories.

The seven explicit categories according to the enrolled text are:

- public safety (police, fire and emergency medical services);

- education and public schools;

- infrastructure (construction and maintenance of roads, bridges and storm water control);

- natural resource projects including flood control;

- municipal bonds and payment of existing debt;

- retirement benefits for local government employees;

- and the operations of county officials and municipalities pursuant to Article VIII of the Florida Constitution.

The practical extent of this restriction depends on how the seventh category is interpreted.

The enrolled text of CS/HJR 1F includes in that category not only the institutional operations of county officers but also “the expenditures approved by such county officers or county or municipal governing bodies, except those expenditures prohibited by general law.”

That clause introduces a legal ambiguity of consequences not yet publicly analyzed in detail: a local government could argue that any expenditure approved in the regular budget process -cultural grants, grants to non-profit organizations, economic development programs- falls under that seventh category.

Under a more restrictive interpretation, the previous six categories would be exhaustive and the seventh would cover only the institutional operation of the government apparatus, which would leave without explicit constitutional basis the financing of discretionary programs via ad valorem tax.

The January 28, 2026 Florida DOGE report accurately audited the operations of county and municipal officials.

For Broward County, the report documented a 65 percent increase in cultural grants-from FY 2021-22 to $9.2 million in FY 2024-25-and the allocation of $175,000 to a virtual art project accessible only through the Metaverse. For Orange County, it documented $80 million in grants to nonprofits as a category of spending classified as excessive.

For Miami-Dade County, the section operates in two scenarios.

- 1- If the amendment does not reach the 60 percent threshold by November 2026, Section 9(2) does not take effect: CS/HJR 1F is a unified proposal that requires full ratification by the electorate.

- 2- But if approved, the use restriction becomes the constitutional architecture that frames how the county can use the property tax during the transition phases to the expanded exemption.

DeSantis’ argument: real savings for the homeowner and spending problem, not revenue problem

For Governor DeSantis and proponents of the proposal, the starting point is not the county budget but the homeowner’s pocketbook. The post-COVID real estate boom raised property values by 40 to 80 percent in many Florida markets between 2020 and 2024. Although the Save Our Homes mechanism limits the annual increase in assessed value to 3 percent for homestead properties, homeowners who bought in recent years entered the market with already inflated base values and significantly higher tax bills than their neighbors with similar but older-owned properties.

The official SaveOurHomesFL.com calculator, launched on June 1, 2026 simultaneously with the opening of the special session, allows each homeowner to enter their address and view three pieces of information: current 2025 tax, projected tax with $250,000 exemption, and estimated annual savings.

On a $350,000 homesteaded home in Broward County, the calculator projects a reduction in the non-school bill from $6,115 to $3,443, a savings of $2,672 annually. According to the governor, approximately 60 percent of homestead exemption homeowners in Florida would pay zero in non-school property taxes by 2028 if the amendment is ratified.

The governor’s fiscal argument is structural: local governments do not have a revenue problem but an expenditure problem. Under that thesis, the growth in assessed values generated an automatic increase in revenue that local governments absorbed by expanding their budgets, and the proposal forces them to operate at efficiencies comparable to the pre-inflation period. An administration spokesperson told PolitiFact that claims that the proposal would “defund” essential services are false, and that municipalities can absorb the revenue reduction given how much their revenues have grown in recent years.

To support that framework, the administration launched Florida DOGE, a local budget audit initiative spearheaded by CFO Blaise Ingoglia, in 2025.

The report released on January 28, 2026 -99 pages- identified $1.86 billion classified as “excessive spending” in the audited budgets of Florida counties and municipalities, without detecting criminal fraud.

The local governments audited rejected the characterization: they argued that the expenditures identified respond to legitimate programmatic mandates approved in a public and open budget process.

The spending argument has indirect support from within the Miami-Dade Board of County Commissioners itself. Commissioner Vicki L. Lopez D5 – former chair of the Property Tax Committee in the Florida House and BCC’s legislative bridge in Tallahassee – noted in the March 17, 2026 hearing, in reference to the state legislative budget, that the Florida House presented that year “a strong fiscal conservative budget that did not reduce services,” while the Senate proposed a budget of nearly $1 billion more.

The majority bloc that approved the amendment was not monolithic in its positions. Republican Senator Ed Hooper (Dist. 21), Chairman of the Senate Appropriations Committee and one of the affirmative votes on June 2, raised during the debate a structural concern about the unequal distribution of the impact among jurisdictions: “There’s 67 totally different counties in this state, and a property tax issue that is great for one county could crush 31 poor counties.” His vote in favor of the final text suggests that this concern was not determinative against the proposal as a whole.

The political dynamism of the proposal reflects its transpartisan appeal. Three Democratic senators crossed party lines to vote in favor. Mack Bernard, who represents the West Palm Beach area of Palm Beach County, was also a co-introducer of the Senate version of CS/SJR 2-F along with Senator Avila and Senator Debbie Mayfield (R-Brevard). Daryl Rouson of St. Petersburg in Pinellas County and Barbara Sharief of Miramar in Broward County also voted yes. Their affirmative vote is notable against the position of their co-religionist Sen. Lori Berman, who called the proposal “a political stunt.”

Miami-Dade as a case study: debate on the Senate floor

During debate on the floor of the Florida Senate on June 2, 2026, three senators from the Miami-Dade area-two Republicans and one independent-voted in favor of the amendment and made the county the central example of their argument: the problem is not a lack of revenue but overspending.

The Miami Herald documented the exchange in its June 5, 2026 edition (Garrett Shanley and Douglas Hanks) under the headline“Florida lawmakers describe Miami-Dade as the poster child for wasted tax dollars.”

Sen. Bryan Avila (R-Miami Springs), lead sponsor of CS/SJR 2-F, articulated the structural argument:

“Miami-Dade County government is showing signs of a system under strain. Years of neglect, mismanagement, and shortsighted decision-making have left some of our most important public assets and services facing serious challenges.”

Avila further noted that the county had put off addressing a projected $400 million budget shortfall, summing up the situation with the phrase, “Only in Dade.” On the details of the spending, Avila cited vehicles assigned to the commissioners’ security staff:

“Many of them have, essentially, a full-time sergeant-at-arms in a Grand Wagoneer.”

Sen. Ileana Garcia (R-West Miami, District 36), R-Miami-Dade, was more direct about the role of these security agents, describing them as “bodyguards” and “UberEats” to the commissioners, and questioned the county government’s lack of fiscal action:

“I never saw any of them in Miami-Dade County go in and try to cut out some of the fat that they had in their budgets.”

Senator Jason Pizzo (Independent, former Democrat from the North Miami-Dade area) extended the criticism to other discretionary spending items:

“I think it’s pathetic what Miami-Dade spends on. I don’t want to see trips to Qatar and parades and stages and all these events anymore.”

In his closing remarks to CS/SJR 2-F, Senator Avila offered a historical argument that placed the current homestead exemption in long-term perspective. Using state data, he traced the trajectory of the percentage the exemption represented of the typical value of a Florida home from its inception in the 1940s to the present – an argument aimed squarely at those who labeled the proposal as unprecedented (Source 56, timestamps 3:32:16-3:34:52):

“In the 1940s, when the first property, Homestead Property Tax Exemption came into place, it was for ,000. That made up over 225.4% of the Homestead Exemption compared to the [home value]. Meaning that there were a lot of Floridians in the 1940s that were not paying property tax. As the years kept going, the state kept growing. In the 1950s, that percentage went down to 75.6%. In the 1960s, it went down to 42.4%. When we got to the 1980s, I’m sure that legislature had a similar conversation to the one we’re having. “

“And I say that because the property tax exemption went up from $5,000 to $25,000. And that brought the percentage back up to 55.4%. 1990, that percent came down to 32.4%. 2000s, it came down to 23.7%. In the 2010 years, the legislature at that time must have had a similar conversation to the one we’re having. Because that’s when the additional $25,000 Homestead Exemption came into place. And that additional $25,000 brought the percentage just slightly to 24.3%. Fast forward a number of years to present day, and we’re well under 16%. 16% is what our residents are saving with regards to their taxes with the Homestead property tax exemptions we have right now in place.”

In the same closing remarks, Avila identified by name the three counties among the eight that exceeded 100 percent of the maximum millage rate – Miami-Dade, Broward and Palm Beach (Source 56, timestamps 3:40:12-3:41:26):

“Out of the 67 counties, nine of them, and I mentioned this yesterday, nine of them voted to keep their millage either at the rollback rate or below. Just nine of them. Fifty of them raised taxes on our residents with a simple majority vote. Eight of them went even further. Eight of them went up to over 100% of the maximum millage rate. No surprise my county is one of those eight. So is Broward. So is Palm Beach. How can we explain that? I have no explanation for it. Those three counties have seen substantial investment and commercial base expansion. I can’t explain.”

On municipalities, Avila extended the argument to the city level:

“If you want to go down to the city level. 117 municipalities. 117 municipalities. They increased their taxes up to that 110%. And 11 of them went above with a unanimous vote. Went above 110% in terms of taxes.”

During the debate, legislators also presented county payroll data to illustrate the scale of administrative spending.

Among the items noted: Miami-Dade County employs at least 12 social media specialists spread across public safety and service departments, with annual salaries ranging from $69,334 to $127,057, according to public county payroll records.

| Department | post | Annual salary |

|---|---|---|

| Comm, Information & Technology | Com Social Media Coordinator | $127,057 |

| Aviation | Senior Social Media Specialist | $107,592 |

| Fire Rescue | Senior Social Media Specialist | $102,790 |

| Seaport | Social Media Manager | $101,187 |

| Transportation & Public Works | Social Media Manager | $101,187 |

| Transportation & Public Works | Senior Social Media Specialist | $95,814 |

| Aviation | Senior Social Media Specialist | $91,461 |

| Libraries | Social Media Specialist | $91,461 |

| Community Services | Social Media Specialist | $79,628 |

| Water and Sewer | Senior Social Media Specialist | $75,988 |

| Corrections and Rehabilitation | Senior Social Media Specialist | $75,832 |

| Parks, Recreation & Open Spaces | Social Media Specialist | $69,334 |

Source: Miami-Dade County public payroll records, verifiable on the county’s salary search portal(miamidade.gov); data displayed on the floor of the Florida Senate during the June 2, 2026 special session.

The legislators’ display of this salary data was used as a political argument about the scale of the county’s administrative spending; their inclusion in this piece does not imply that the positions are irregular or that their holders have incurred in any irregularity whatsoever.

The Cava administration responded to the senators’ questioning with a statement quoted by the Herald: “Miami-Dade continues to operate a lean, efficient government.” The county government pointed to having reduced the millage rate in four consecutive fiscal years to its lowest level since 1982, cut executive salaries, consolidated departments and eliminated positions.

The $473 million shortfall and the law the county ignored from 2018.

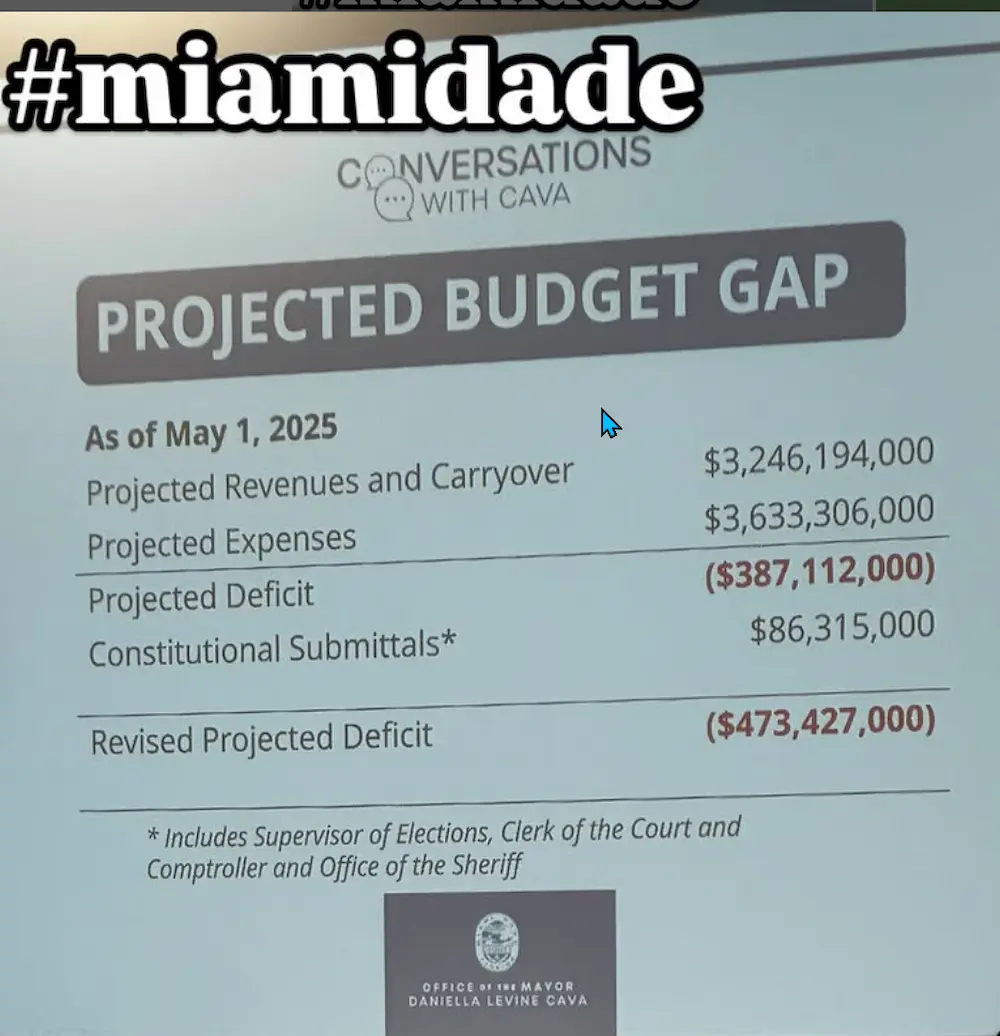

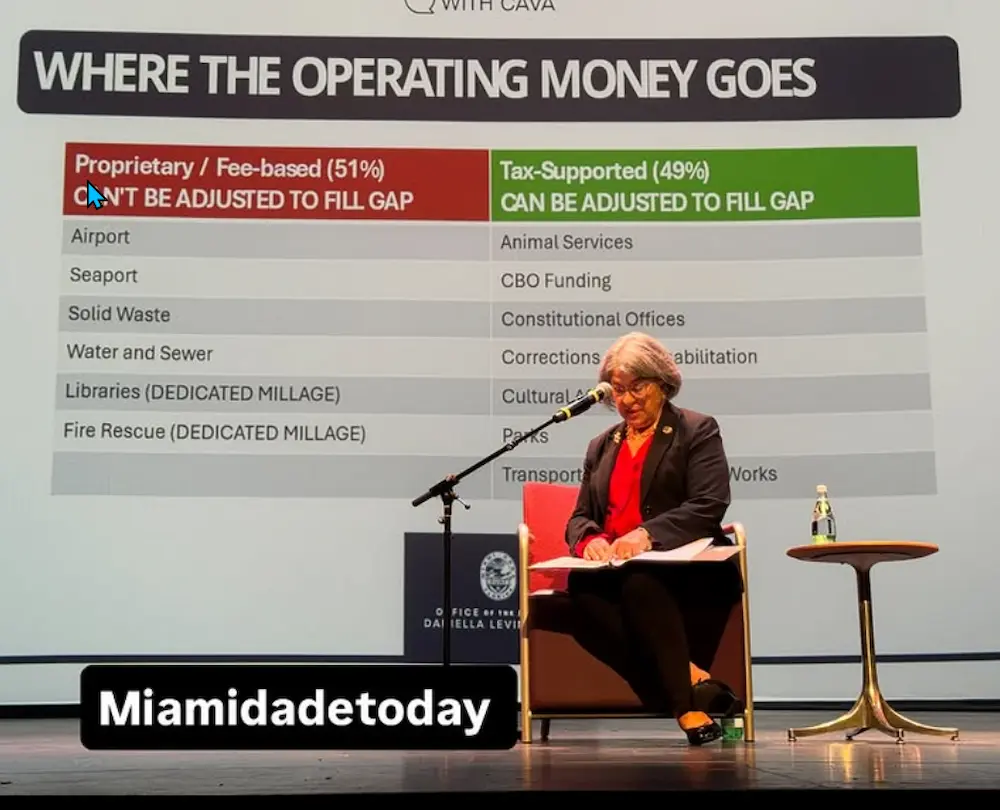

On September 18, 2025, during the second Fiscal Year 2025-26 budget hearing before the Board of County Commissioners, Mayor Levine Cava presented a slide from the“Conversations with Cava” cycle containing a radically different distribution of responsibility from her public narrative.

According to that official mayoral document, the county projected revenues and carryover of $3,246,194,000 versus expenditures of $3,633,306,000 for that fiscal year, generating a base deficit of $387,112,000 -attributable to the county administration’s own spending decisions.

The independent constitutional offices (Supervisor of Elections, Clerk/Comptroller and Sheriff) added an additional $86,315,000 in their mandatory submittals.

The resulting revised deficit: $473,427,000.

The breakdown is unambiguous: 81.8 percent of the deficit was generated by the county administration’s spending decisions; 18.2 percent was accounted for by submittals from the three constitutional offices. At that same hearing, the independent constitutional offices returned unspent funds to the county: the Tax Collector’s Office returned $13.5 million and the Clerk/Comptroller returned an additional $5.3 million, according to that session’s budget record.

Major Cava has attributed part of the structural deficit to the creation of Miami-Dade’s five independent constitutional offices-Sheriff, Property Appraiser, Tax Collector, Supervisor of Elections and Clerk of Courts/Comptroller-established by state law in 2018.

The chronological problem with that argument is that the law that created the independent constitutional offices was enacted in 2018. Seven fiscal years elapsed between the enactment of the law and Fiscal Year 2025-26. The county administration had seven years to prepare for the budget transition. The law was not a last-minute surprise.

The data that contextualizes that shortfall comes from Florida DOGE itself: between Fiscal Year 2016-17 and Fiscal Year 2024-25, the county’s General Fund grew by 82.5 percent. Over that same period, the county’s population grew by less than 3 percent. The county’s overall spending grew approximately 27 times faster than its population.

The report itself stated that the mayor had announced the deficit “despite tremendous growth in revenues and spending over the past few years” – a qualification by the state fiscal agency that frames the budget gap as the result of spending growth, not revenue shortfalls.

The January 2026 Florida DOGE report devoted pages 56 to 60 of its 99 pages to Miami-Dade County.

One fact that the report explicitly notes that distinguishes Miami-Dade from the other twelve jurisdictions examined: “no site visit performed to date.” Unlike Orange County, Jacksonville, Broward and the other nine local governments where the DOGE team conducted site visits, Miami-Dade’s analysis relied exclusively on public documents and data provided by the county itself.

This methodological limitation did not attenuate the conclusions.

The report identified 26 expenditure items classified as excessive – without pointing to criminal fraud – and documented a systematic pattern in contracting: “dozens of engineering services contracts for $999,999.90,” ten cents below the $1 million threshold requiring approval by the Board of County Commissioners.

The report calls that pattern“excessive structuring of contracts to avoid the need for public transparency and Board of County Commissioners consideration.”

THE 26 EXAMPLES OF “EXCESSIVE SPENDING” – Complete List

| # | Example | Amount |

|---|---|---|

| 1 | approximately $9.6 million in payroll in the Mayor’s Office for approximately 50 positions. | $9.6M |

| 2 | “Art Allowance” new detention center. 9 million in art for county’s new detention complex | $9M |

| 3 | Office of Community Advocacy | 19 FTEs |

| 4 | Cultural Grants DEI-themed | $13.7M |

| 5 | Federal grants consulting (5 years) | $10M |

| 6 | County Attorney’s office growth | 146→168 FTEs + $300K+ salaries |

| 7 | Art in Public Places ordinance | $17M+/year |

| 8 | Legal aid + $100M rolled over | $4.4M |

| 9 | Cultural Affairs general fund + CDT/TDT | $14.5M + $29M |

| 10 | ICLEI membership | $14K |

| 11 | “Tree equity. 500,000 in a program called “tree equity, | $500K |

| 12 | Curbside recycling (7% of waste) | $13M |

| 13 | Office of New Americans | $2M |

| 14 | Vehicles Community Action | $120K each |

| 15 | Among the expenditure items linked to climate initiatives, “Extreme weather training”, “Extreme weather training | $220K |

| 16 | Bus cleaning COVID standards. A $24.1 million recurring contract for bus cleaning under COVID disinfection standards. | $24.1M ongoing |

| 17 | Mental health “social justice” consulting | $250K non-competitive |

| 18 | Transit “mobility reward | $430K |

| 19 | $999,999.90 contracts pattern | structuring |

| 20 | SMART transit future subsidies | $100M/year future |

| 21 | Capital spending doubled | $2.3B→$4.7B |

| 22 | Cultural Affairs capital: On the capital side, the report documents that total county capital spending doubled in less than a decade: from $2.3 billion in FY 2016-17 to $4.7 billion planned for FY 2025-26. Increases include: art in public buildings from $8 million to $93 million; | $8M→$93M (+1,062%) |

| 23 | Library capital: library capital from $11 million to $41 million; | $11M→$41M (+273%) |

| 24 | Seaport capital: and the Seaport’s capital budget, which went from $136 million in 2017 to zero dollars planned for FY 2025-26. | $136M (2017) → $0 (FY25-26). |

| 25 | Shore power + FPL guarantees: the report also identifies a project to supply electricity from the cruise ship dock at PortMiami, valued at at least $125 million; the county assumes revenue guarantees payable to Florida Power & Light of up to $18 million over four years if the infrastructure is not sufficiently utilized – a risk the report itself describes as likely given that shipping lines are “reluctant to use shore power due to high costs relative to ordinary diesel operations.” | $125M + $18M |

| 26 | Proterra buses + South Dade Corridor: and losses in the operation of Proterra brand electric buses – approximately 72 units at more than $1 million each, “largely idled” – that were to be replaced by New Flyer units for the South Dade Corridor, opening in October 2025 at a cost of more than $300 million. The general fund’s annual operating subsidy to the county’s transit system amounts to $270 million, according to the same report. | ~$72M + $300M + $270M/yr subsidy |

The most serious finding in the Miami-Dade chapter is not any specific expenditure line item. It is the response the county administration gave to the DOGE team when it requested that the county indicate where in the budget a subset of contracts valued between $75,000 and $5 million were authorized.

The response, reproduced verbatim in the official report: “That would require a Herculean effort,” because the county “doesn’t think about” spending in those terms. The report concludes that “awarding contracts without directly considering whether those contracts support the objectives of the County’s elected Board of County Commissioners and have been appropriately funded through the annual budgetary process renders irrelevant the efforts by citizens and elected officials to combat waste and ensure that taxpayer funds are being put to appropriate use.”

The report also documented the magnitude of the revenue increase that made that spending expansion possible: between Fiscal Year 2021-22 and Fiscal Year 2023-24, Miami-Dade’s property tax revenues grew by $431 million, 29 percent, even after the millage was reduced by 2 percent during that period. In the same interval, the library budget grew by 31 percent, about $23 million more per year. The report concludes that “the scale of this growth has enabled a remarkable amount of irresponsible spending, when the County should have prioritized limiting the burdens of rising property values on county taxpayers.”

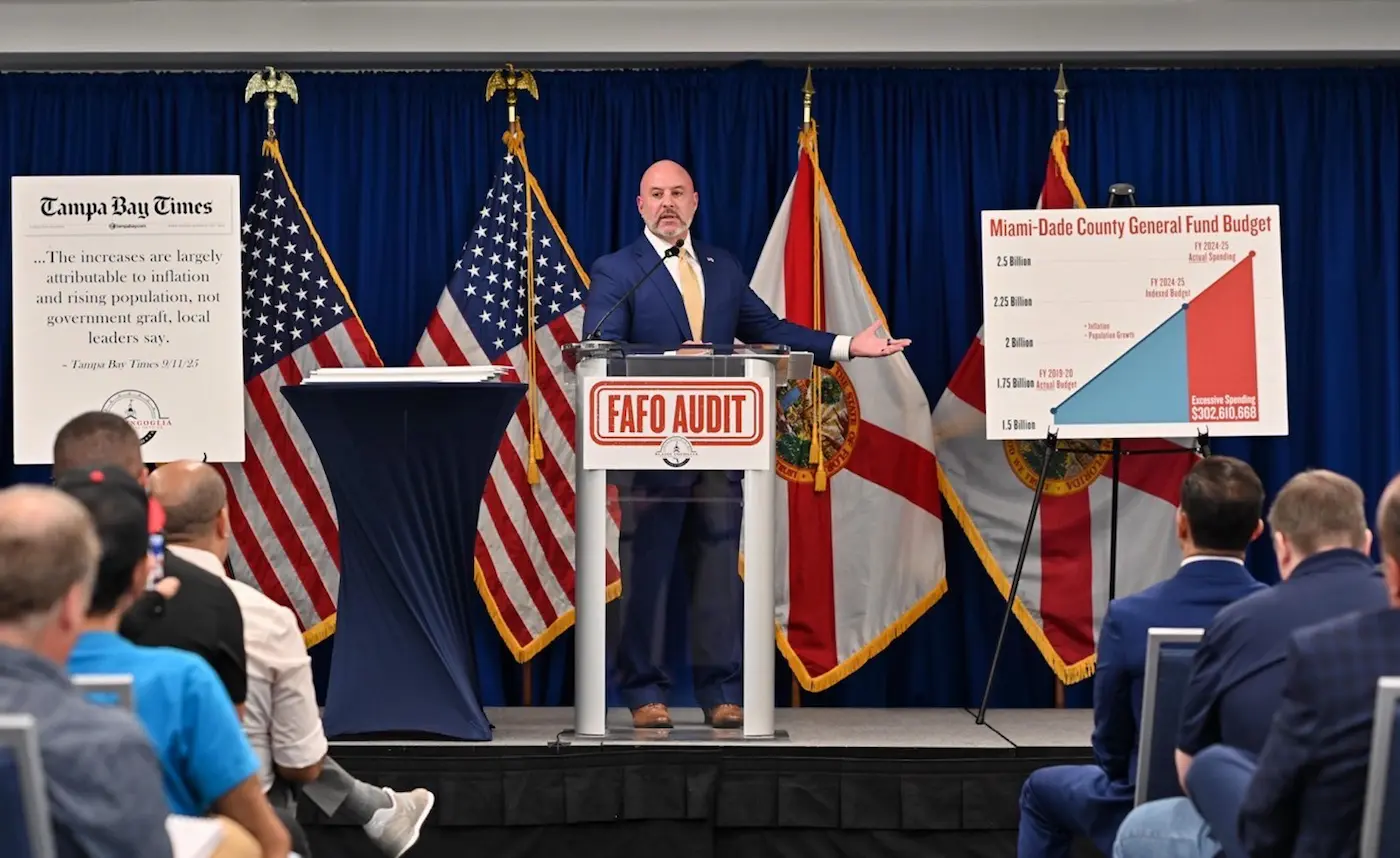

On June 11, 2026, three days prior to the publication of this piece, CFO Blaise Ingoglia again singled out Miami-Dade with an updated figure. In an official release, the Florida Department of Financial Services reported that the Florida Agency of Fiscal Oversight – FAFO – identified more than $470 million in Miami-Dade County’s FY 2025-26 budget as “excessive, wasteful spending.” According to the release, FAFO also concluded that the county’s budget increased by $1.078 billion, while the population grew by 5.72%, and that the county could reduce the millage by 0.83 mills without affecting critical services.

Added to the $302 million identified the previous year and the findings from the year before that, the total overspending in Miami-Dade over the past three years amounts to $807,361,670, according to agency records.

CFO Ingoglia quantified the margin of adjustment available without affecting essential services: the county could reduce its millage rate by 0.83 mills. That reduction would imply annual savings of $413 for a property with a taxable value of $500,000, $496 for a $600,000 property, and $579 for a $700,000 property. The FAFO recommendation is the first time a state agency has quantified a specific millage cut for Miami-Dade without conditioning it on loss of services.

In the FY 2025-26 budget process record, the county operating millage remained at 9.5778 – identical to the previous fiscal year – while assessed values grew 5.5 percent. A frozen millage in an environment of rising values is tantamount to a decision to capture the automatic increase in collections rather than return it as a reduction in the bill. Based on verified data from the six adopted budgets, all FY 2025-26 county levies passed above the rollback rate-the rate that would have kept collections at the same level as the previous year without capturing the growth in assessed values.

Gonzalez-Cava clash and Sen. Garcia’s motion at the budget hearing

The argument that Miami-Dade has a spending problem, not a revenue problem, didn’t come first from Tallahassee. It came from the Board of County Commissioners’ own dais, in the voice of Commissioner Roberto J. Gonzalez (D11), during the second budget hearing on September 18, 2025 – the same event where the Major presented the $473 million deficit.

Gonzalez took the floor after other commissioners had presented their own questioning and began with a reminder of who depends on the budget: the residents who came at rush hour to speak for a minute, and those who couldn’t come – “the mom who works two jobs to make ends meet and can’t come speak because she can’t get somebody to watch her kids.” Then came the direct accusation:

“I’m disappointed with the mayor and her team for the utter lack of information and transparency during the entire budget process. I’ve spent months trying to get answers to simple questions.”

Gonzalez accused the administration of operating in a systematic pattern of withholding information:

“The lack of information and transparency is designed to lead toward a predetermined outcome. Each of us at one point or another has experienced and made comments from this dais about how we are dissatisfied with the administration’s tactics of delivering information at the last minute. That’s if they deliver it at all. And yet we’re kept in the dark. We’re kept in the dark by an administration that does not respect the role of this commission.”

The commissioner evoked the Florida DOGE report and projected it directly onto Miami-Dade:

“We saw how state CFO [Blaise Ingoglia] and Florida DOGE found over $200 million in overspending in Orange County and Jacksonville. And what I pose to all of my colleagues is imagine what they could find or will find in Miami Dade County.”

On that day, Gonzalez presented a document of proposed cuts that he described as the most detailed ever delivered at that hearing. He identified line item by line item the expenses he felt could be eliminated and redirected to reduce the millage rate: $21 million from the overall budget earmarked for the FIFA World Cup – which he felt should be funded by tourism funds rather than property tax – and $7.26 million that the administration had absorbed by “eliminating” the Office of Resiliency but reallocating its 10 positions to DERM. About FIFA:

“Commissioners, there is no reason why taxpayers should pay $21 million for the World Cup when we have tourist tax money that should be used for that purpose.”

About the Office of Resilience absorbed by DERM:

“If the mayor claims to have cut the office of resilience that she respectfully created, then why does [DERM] have a $7.26 million absorbing 10 positions from the Office of Resilience?”

The sum of the cuts proposed by Gonzalez at that hearing-FIFA, DERM/Resilience, a new creative services division in Communications, vacant marketing positions, environmental program advertising that staff could not account for, positions in Solid Waste and Water and Sewer, plus the formally eliminated but still funded fluoride budget-would, by his estimate, add up to enough to reduce the county’s operating millage from 4.5740 to 4.4919:

“We can lower the millage rate to 4.4919, which is a 1.8% cut. This is a fair amount and a bold move toward alleviating the tax burden on Miami Dade County residents.”

González closed his speech with an accusation of institutional contempt:

“The utter lack of transparency, the unclear answers, the misdirection, this cannot continue because it’s a great disservice and an utter attack of regard and respect to our office and the people we represent.”

Major Cava responded immediately. His tone was as direct as that of González. First he questioned the commissioner’s knowledge:

“This unfortunately demonstrates the lack of knowledge of the budget process by this particular commissioner. This is a collaborative process. I have met with every single commissioner multiple times. Unfortunately, this commissioner repeatedly declined those meetings or canceled them at the last minute to score political points.”

He then responded point by point to some of the accusations – the Office of Resilience was created by his predecessor, FIFA was approved by this same BCC – and closed with a warning about institutional hierarchy:

“You do need to show me respect. And per the charter, I am the mayor. I was elected by the people of this county, not once, but twice because they trust me.”

At the same hearing on September 18, then Senator René García – at that time State Senator for District 36, later elected to the BCC as D13 Commissioner – made a formal motion that was seconded by Commissioner Gilbert.

The motion proposed:

- reduce US$383,000 in travel expenses

- and registration distributed to the Mayor’s Office ($6,000),

- Corrections ($109,000),

- Medical Examiner ($70,000),

- Emergency Management (US$8,000),

- Transportation and Public Works ($122,000),

- Miami-Dade Economic Advocacy Trust ($3,000),

- Community Services ($41,000)

- and Cultural Affairs (US$24,000).

Garcia added:

the elimination of one administrative vacancy in HR – a recruitment manager position valued at $187,200 – for a total of $570,200 reallocated to four nonprofit organizations: $126,200 to Voices for Children Foundation, $100,000 to Farm Share, $200,000 to the Cuban American Bar Association Pro Bono Project and $144,000 to the Miami-Dade Mental Health Advisory Board.

Garcia’s argument to his colleagues was pragmatic:

“If we are reducing travel, like the mayor says, we’re reducing travel. So that means we don’t need as much money in those accounts. There is enough money in those accounts that we’re taking a little bit from all of them to make sure that we make these organizations whole.”

About the HR vacancy it eliminated:

“If we are already in the process of doing this pipeline and making sure that employees go somewhere else and there’s a hiring freeze, why are you going to tell me that we need this recruitment position at this $187,000 value?”

The September 18, 2025 clash between Gonzalez and Cava – and Garcia’s motion – documents that the debate over whether Miami-Dade has a spending or revenue problem did not begin on the floor of the Florida Senate in June 2026. It was already on the BCC’s table nine months earlier, from within the county government itself.

South Florida’s most expensive county salaries: why officials fear reform

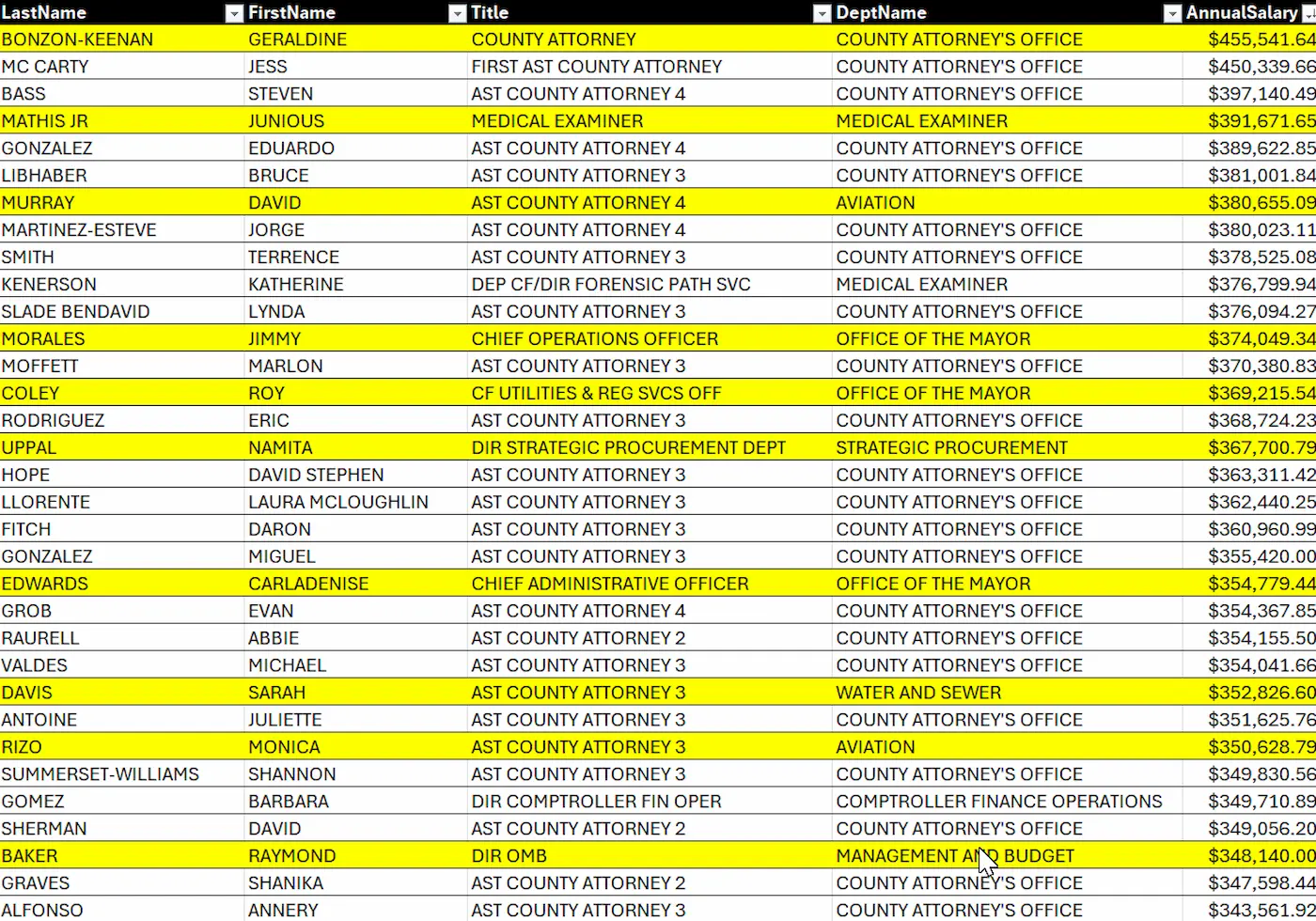

The debate over whether Miami-Dade has a revenue or spending problem has a specific dimension that has not appeared in the county administration’s public communications against the DeSantis proposal: the salaries of its own officials. According to public county payroll records verified by News Miami Dade – data accessible on Miami-Dade County’s public payroll portal,

snapshot of June 2, 2026- County Attorney Geraldine Bonzon-Keenan receives an annual salary of $455,541.

- His first assistant, Jess McCarty, is paid $450,339.

- The Director of the Aviation Department, Rafael Cutie, receives US$408,402.

- The current former Chief Operations Officer of the Mayor’s Office, Jimmy Morales, receives US$374,049.

- The FY 2025-26 adopted budget records 31,996 total positions in the county.

Miami-Dade County Employee Compensation Information 2026

The benchmark comparison of salaries at different Federal, State, County and City levels is of direct relevance:

- The official salary of the president of the United States – including Trump while in office – is: $400,000 per year, paid monthly. The official source is U.S. Code, Title 3, Section 102, which states that the president receives $400,000 per year and, in addition, an expense allowance of $50,000 for expenses related to his official duties.

- The County Attorney of Miami-Dade County is paid $55,541 more per year than the President of the United States.

- The First Assistant County Attorney is paid $50,339 more.

- The Director of Aviation is paid $8,402 more.

All three are civil servants paid primarily with the ad valorem tax that the county administration defends before the Florida Legislature.

- The comparison is magnified when the City of Miami is included as a separate municipal entity from the county. The City Manager of the City of Miami, Jems A. Reyes, earns an annual salary of $475,000 according to City of Miami payroll records current as of May 20, 2026-$75,000 per year above the presidential salary.

- The City Attorney of the City of Miami receives $417,642 per year.

The Miami-Dade County Attorney’s Department has the highest salary density in the county payroll: of the 100 highest paid county officials, more than 40 belong to the County Attorney’s Department, with individual salaries ranging from $290,000 to $455,541 per year.

The Mayor’s Office reported to the Florida DOGE an allocation of approximately $9.6 million for about 50 senior positions, which represents an average of about $192,000 per year per position in that subset. These figures are from public records; their inclusion does not imply any wrongdoing on the part of the appointees.

Senator Avila articulated before the full Florida Senate on June 2, 2026 the structural argument underlying this data. In his opening remarks to CS/SJR 2-F, delivered on the Senate floor prior to the vote, Avila stated:

“Senators, property tax collections statewide have almost doubled since the pre-COVID years. Rising from $35 billion in 2019 through 2020 to a projected $62 billion this year alone. That equates to a 77% increase in 6 years. These increases have far exceeded growth in CPI and population. For example, in 2022 through 2023, CPI was 6.3% and property tax collections increased by 12.3%. In 2023 through 2024, the CPI increased by 3.3% and property tax collections increased by 13.9%. Our population increase in those years was between 1.6% and 1.7%.”

Later in the debate, answering questions from colleagues about why the Legislature should intervene in local fiscal management, Avila was more precise about the majority behavior of Florida’s 67 counties:

“Nine of the 67 counties did the right thing as a resident and went to the rollback rate or below the rollback rate. Meaning that the overwhelming majority of those 67 counties didn’t do the right thing and they raised taxes on our residents. Mind you, these past three years for the overwhelming majority of counties, they’ve seen an influx in commercial and residential revenue.”

In his closing remarks the same day, Avila reiterated that statistic and identified by name the three counties that exceeded 100 percent of the maximum millage: Miami-Dade, Broward and Palm Beach (Source 56, timestamps 3:40:12-3:41:26).

Miami-Dade County is not among the nine counties that went to the rollback rate. Its operating millage remained identical to the previous year while growth in assessed values automatically generated more revenue. The implicit question Avila left open on the Senate floor – and one that resonated with the DOGE, deficit report and county payroll data – is whether a local government system that grows its overall spending 82.5 percent in eight years, while its population grows less than 3 percent, does indeed have a revenue problem.

Why it matters

Florida is one of nine states without a state income tax. Its tax model rests on three structural legs: state sales tax, property tax administered by counties and cities, and tourism-related taxes.

The property tax accounts for 74 percent of Florida’s local tax revenue and primarily supports municipal and county services and school districts.

For Miami-Dade County, approximately 33 to 40 percent of the county’s general fund comes from ad valorem property tax.

According to the revised 2024-2026 tax rankings, no state is listed as having completely eliminated the homestead property tax. Hawaii records the lowest effective rate in the country, at about 0.29 percent, followed by Alabama, at about 0.37 percent; both states continue to levy the tax. If the constitutional amendment is ratified in November 2026 and the Florida Legislature complies with the mandate to engineer total elimination by general law, Florida would combine the absence of state income tax with the elimination of the property homestead tax, an unprecedented combination in U.S. tax history.

The magnitude of the revenue replacement problem is illustrated by the extreme scenario: if Florida were to eliminate its property taxes altogether and replace them entirely with sales tax, the Tax Foundation estimates that the state sales tax rate would have to rise from the current 6 percent to 15.34 percent. That scenario is not in the current proposal, but it illustrates the scale of the implied tax trade-off.

Impact estimates for Miami-Dade vary by methodology and scenario: Major Daniella Levine Cava quantified in op-ed published in the Miami Herald during May 2026 that the amendment would cost Miami-Dade approximately $386 million in 2027 and $697 million cumulatively over the first two years. Miami-Dade County Property Appraiser Tomás Regalado raised that figure to approximately $925 million over the same two-year period according to NBC Miami data. Regalado called the proposal “the most important and momentous vote in many decades” for Florida.

The Miami-Dade Property Appraiser’s Office separately projected the average savings per homestead owner: nearly $1,700 in 2027 – with a reduction in county revenue of $130 million that year – and nearly $2,800 in 2028. Carlos Migoya, outgoing CEO of Jackson Health System, quantified a specific impact of $83 million annually on the county’s public health system, according to the Board of County Commissioners’ verbatim transcript of March 3, 2026:

“If enacted, that proposal could negatively impact Jackson by approximately 83 million a year.”

At the statewide level, official legislative estimates project a revenue loss to local governments of $4.6 billion in 2027 growing to $8.4 billion in 2028. The Florida Association of Counties estimates that, if the full elimination of the property tax homestead were completed in later phases, the statewide impact would reach $8.65 billion annually.

Property tax as a pillar of the county budget: millage fell 2 percent in five years – revenue up 55 percent

To understand the scale of the debate, it is useful to view the property tax not as a line item in the budget but as the pillar that supports it. The tax-supported portion of Miami-Dade County’s budget-the Countywide General Fund, the UMSA General Fund, the library system and the Fire Rescue Service District-totaled $3.883 billion in FY 2024-25 and $4.266 billion in FY 2025-26, with ad valorem as its primary funding source. That block represents the county spending most directly affected by the amendment: it pays for police, transit, parks, social services and basic infrastructure that residents receive without paying a ticket.

The county’s total adopted budget grew from $9.052 billion in FY 2020-21 to $13.233 billion in FY 2025-26, a 46.2 percent increase over five fiscal years. Within that total, the tax-supported portion grew from $2.737 billion (FY 2020-21) to $4.266 billion (FY 2025-26), an increase of 55.9 percent. Verified data from the six adopted budgets show the full trajectory:

| Fiscal year | Total budget adopted | Property tax collection | Total county millage | Invoice example UMSA |

|---|---|---|---|---|

| FY 2020-21 | $9,052M | $2,094M (37%) | 9.7779 | $2,650 total / $1,467 county |

| FY 2021-22 | $9,302M | $2,187M (39%) | 9.8074 | $2,642 total / $1,471 county |

| FY 2022-23 | $10,400M | $2,419M (36%) | 9.6922 (1st cutoff) | $2,624 total / $1,453 county |

| FY 2023-24 | $11,764M | $2,702M (37%) | 9.5962 (2nd cut) | $2,542 total / $1,438 county |

| FY 2024-25 | $12,760M | $2,991M (37%) | 9.5878 (3rd cut) | $2,540 total / $1,437 county |

| FY 2025-26 | $13,233M | $3,251M (38%) | 9.5778 (4th cut; frozen operating millage) | $2,538 total / $1,436 county |

| Variation 5 years | +$4,181M (+46.2%) | +$1,157M (+55.2%) | -0.2001 mills (-2.0%) | -$112 total (-4.2%) |

Sources 37, 42, 43, 44, 36, 45. The “sample UMSA bill” corresponds to the projected tax on a $200,000 market value home with a taxable value of $150,000 (after standard $50,000 homestead exemption) in the Unincorporated Municipal Service Area.

The most telling fact in that table is not the growth in the total budget but the divergence between the millage column and the property tax revenue column. The county’s total millage fell from 9.7779 mills in FY 2020-21 to 9.5778 mills in FY 2025-26, a reduction of 0.2001 mills equivalent to 2.0 percent. Over the same period, adopted property tax collections rose from 2.094 mills to 3.251 mills, an increase of 55.2 percent.

The county reduced its tax rate in terms of millage, but assessed values of Miami-Dade properties soared enough that collections grew anyway and steadily – 55 times faster than the rate cut.

The example bill column shows a downward trajectory: from $2,650 in FY 2020-21 to $2,538 in FY 2025-26, a reduction of $112. That benchmark is the story the county administration publicly presents as evidence of its tax relief policy: the homestead owner with seniority pays less today than he did five years ago. But the benchmark uses a fixed taxable value.

In reality, a homeowner who bought in 2022 or 2023 at the inflated market prices entered the system with a significantly higher base value than his neighbor with the same property but owned for more years, protected by the Save Our Homes cap. For that recent buyer, the bill did not go down $112: it went up in proportion to what he paid for the property. For renters, the benchmark is irrelevant: they are not homestead owners, and their rents rose in step with the market appreciation that drove the county levy.

The most significant piece of data for discussion heading into November is the slowdown: Miami-Dade’s taxable value, which reached an estimated $540.7 billion as of June 1, 2026, is now growing at 5.5 percent – half the rate of 2024. That means that even without the amendment, the county’s tax margin narrows.

Timeline: from state campaign to November 3, 2026 ballot

The proposal to eliminate the property tax in Florida did not emerge in the June 2026 special session. Its trajectory spans three years of legislative evolution, failed negotiations and executive reactivation.

In 2024, Governor DeSantis began publicly articulating the elimination of the property tax as a policy proposal during his Republican presidential campaign. The proposal gained traction in the Republican primary cycle although it did not advance legislatively that year.

In the 2025 legislative session, the bipartisan statewide property tax reform committee produced a slate of seven proposals (HJR 201, 203, 205, 207, 209, 211, 213) that were discussed at the start of the 2026 session. None fully advanced that year. Concurrently, the administration launched the Florida DOGE to audit local budgets as a first step in its tax reform strategy.

On February 2, 2026, at the Miami-Dade Board of County Commissioners Policy Council meeting, Major Cava quantified the potential impact of up to $900 million for the county and began coordinating the institutional response. On March 3, Carlos Migoya of Jackson Health presented to the BCC his quantification of $83 million per year impact on the hospital system.

On March 17, 2026, in a regular BCC session focused on the issue, Commissioner Danielle Cohen Higgins (D8) cited estimates of up to $990 million in potential cumulative shortfall for Miami-Dade. Commissioner Vicki L. Lopez (D5), former chair of the Florida House property tax committee, reported a gap of approximately $1 billion in the state budget and warned of the proposal being blocked in the Senate.

During the 2026 regular session, the House passed HJR 203 by a vote of 80 to 30. The resolution died in the Senate Appropriations Committee without receiving a hearing. The regular session closed without a budget agreement with only 233 bills passed.

In January 2026, the Florida DOGE released its 99-page report identifying $1.86 billion in what it classifies as overspending by local governments. DeSantis and CFO Ingoglia presented the findings as evidence that municipalities have the capacity to absorb a reduction in revenue.

In May 2026, Major Cava published an op-ed in the Miami Herald quantifying the impact of 386 million in 2027 and 697 million cumulatively over two years, and articulated her public position as “tax shift, not tax cut.” This figure is lower than the 900 million estimate Cava had offered in February; the difference reflects that the final legislative text sent to ballot is less aggressive than anticipated at the February Policy Council.

On June 1, 2026, the special session began with the simultaneous launch of the government website SaveOurHomesFL.com, with a $5.5 million earmark for its promotion that opponents called the use of public funds to influence an election referendum. The Senate Appropriations Committee eliminated that line item before the final vote. On June 2, both chambers voted on the same day: the House passed CS/HJR 1-F by a vote of 75 to 26; the Senate passed 30 to 9. The amendment was sent to the November 3, 2026 ballot.

On June 10, 2026, the Appropriations Committee of the Miami-Dade Board of County Commissioners held its meeting, which was the next county institutional milestone on the budget issue.

The opposition coalition: detractors on three fronts

Resistance to the DeSantis proposal was articulated simultaneously on three fronts during 2026: county executives, bipartisan critics in the state Senate and independent tax policy experts. The common point of debate among all detractors is not the individual benefit to the homestead owner-which they recognize as real-but the question of who bears the cost of the services that homeowner uses when his or her contribution to local revenue disappears.

In Miami-Dade, Major Daniella Levine Cava leads the documented institutional opposition. Her opposition strategy combines op-ed in the Miami Herald, formal letter to legislative leaders, direct letter to county union leaders, joint letter to all 34 Miami-Dade municipalities, contracted lobbying in Tallahassee, millage freeze and legislative coordination through Commissioner Lopez. Cava has synthesized his position into the central argument: eliminating the property tax does not eliminate the cost of utilities, it shifts them to tenants, businesses and non-homesteaded property owners.

Jerry Demings, Mayor of Orange County and Democratic candidate for Governor of Florida, articulated the position of county executives with the most direct statement, “This proposal will defund essential public services.”

In the state legislative arena, the most notable opposition was bipartisan. Jeff Brandes, a former Republican state Senator, offered the most succinct criticism from within the party, “This is a tax shift, not a tax cut.” In the House, Republican Representatives Nathan Boyles (Dist. 3) and Patt Maney (Dist. 4) voted against it. In the Senate, the nine “no” votes were all Democrats – Arrington, Berman, Bracy Davis, Davis, Jones, Nathan, Osgood, Polsky and Smith.

The Democratic minority’s legislative strategy did not seek to block the resolution but to amend it. In the State Affairs Committee and on the House floor, Democrats introduced at least ten failed amendments between June 1 and June 2, 2026. The most striking was that of Representative Nixon, who proposed in two versions that “revenue lost by amendments made to this section from the amendment approved by voters on November 3, 2026 will be replaced with a tax on billionaires and any person with over $500 million in assets.”

Other amendments attempted to shield specific services: public libraries (Eskamani), public safety (Cross and Eskamani), veterans’ services (Gantt), senior services (Woodson), children’s services (Bartleman) and water management districts (Cross). Eskamani also introduced a sunset amendment for the constitutional amendment to expire on January 1, 2030. All were defeated on party lines.

On a technical level, the Tax Foundation released an analysis warning that the proposal “would shift property tax burdens in highly distortionary ways” and that it includes “no plan for how to pay for such a large tax cut.” Kurt Wenner of Florida TaxWatch called the impact “so large and unknown” that the actual effects remain uncertain. The Florida Policy Institute warned that landlords would shift the tax burden to tenants through rent increases.

Senators who voted NO and the fiscal realities of their counties

The nine “no” votes in the Florida Senate – all Democrats – represent districts that encompass precisely the counties that Senator Avila identified by name as having raised their millage above 100 percent of the maximum allowed. The geographic overlap between the opposition bloc and the counties with the largest spending expansions is one of the implicit sub-arguments Avila raised on the floor. The table below contrasts the nine senators who voted NO with five who voted YES from South Florida:

| Senator | Party | Dist. | Principal County | Vote |

|---|---|---|---|---|

| Shevrin “Shey” Jones | D | 34 | Miami-Dade | NO |

| Rosalind Osgood | D | 32 | Broward | NO |

| Tina Polsky | D | 30 | Broward / Palm Beach | NO |

| Lori Berman | D | 26 | Palm Beach | NO |

| LaVon Bracy Davis | D | 15 | Orange | NO |

| Kristen Arrington | D | 25 | Osceola / Orange | NO |

| Carlos Guillermo Smith | D | 17 | Orange | NO |

| Brian Nathan | D | 14 | Hillsborough | NO |

| Tracie Davis | D | 5 | Duval | NO |

| Bryan Avila | R | 39 | Miami-Dade | YES |

| Ileana Garcia | R | 36 | Miami-Dade | YES |

| Jason Pizzo | I | 37 | Miami-Dade / Broward | YES |

| Barbara Sharief | D | 35 | Broward | YES |

| Mack Bernard | D | 24 | Palm Beach | YES |

The three Democratic senators who crossed party lines – Bernard (co-sponsor of CS/SJR 2-F), Sharief and Pizzo – respectively represent Palm Beach, Broward and the North Miami-Dade area. The nine “no” votes come entirely from metropolitan counties in the central and southern parts of the state. Tracie Davis, the only senator NOT from a county not among those identified by Avila as over 100 percent of the millage, represents Duval’s District 5 (Jacksonville).

The Cava strategy: nine lines of defense

The Cava administration has deployed since early 2026 a sustained and coordinated response with nine documentable components.

First, op-ed published in the Miami Herald during May 2026 characterizing the proposal as catastrophic. Verbatim quote reported in coverage:

“Eliminating or severely gutting property taxes would be catastrophic for Miami-Dade County. Many renters and business owners could end up paying more despite receiving no direct benefit from a homestead exemption, as higher costs are often passed along through rent increases, fees and higher prices.”

Second, direct post on X reiterating the tax position:

“I believe in tax relief. I have fought for it my entire career. But there is a profound difference between thoughtful tax relief and what is being proposed in Tallahassee right now. Eliminating property taxes is not a tax cut. It is a tax shift that could cost Miami-Dade nearly $700 million in the first two years, threatening essential services that our residents rely on every day.”

Third, formal letter to state legislative leaders urging compromise.

Fourth, a coordinated joint letter with the 34 Miami-Dade municipalities, as cited by Cava in the March 17, 2026 hearing of the Board of County Commissioners:

“We have prepared a joint letter with cities to the legislature. I’ve published an op-ed and I urge all of us to follow through with Jess of course McCarti and also our contract lobbyists to be very active right now.”

Fifth, lobbyist hired in Tallahassee via Jess McCarti (County Intergovernmental Affairs Director) and outside firms. The News Miami Dade database updated as of May 30, 2026 documents 17 individual lobbyists registered with Florida with Miami-Dade County as a client, concentrated in five firms (Corcoran Partners 8 + Continental Strategy 4 + Rubin Turnbull 3 + Oak Strategies 1 + ADF Consulting 1).

Sixth, millage freeze in the FY 2025-26 budget. Major Cava argued at the September 18, 2025 budget hearing:

“Making any millage cuts now when we have prepared a fair balanced budget despite unprecedented financial constraints would be fiscally irresponsible.”

Seventh, coordination through Commissioner Vicki L. Lopez D5 as a legislative bridge. The Chairman of the BCC stated at the March 17, 2026 hearing:

“I am so relieved since you got on the board because you get to deal with Tallahassee now and I’ve actually literally gone much less to Tallahassee since you got on the board.”

Eighth, public alignment with the positions of the Florida Association of Counties (FAC), the Florida League of Cities (FLC) and the Florida Policy Institute (FPI). FAC estimates that, if the total elimination of the property tax homestead were completed in later phases, the statewide impact would reach $8.65 billion annually.

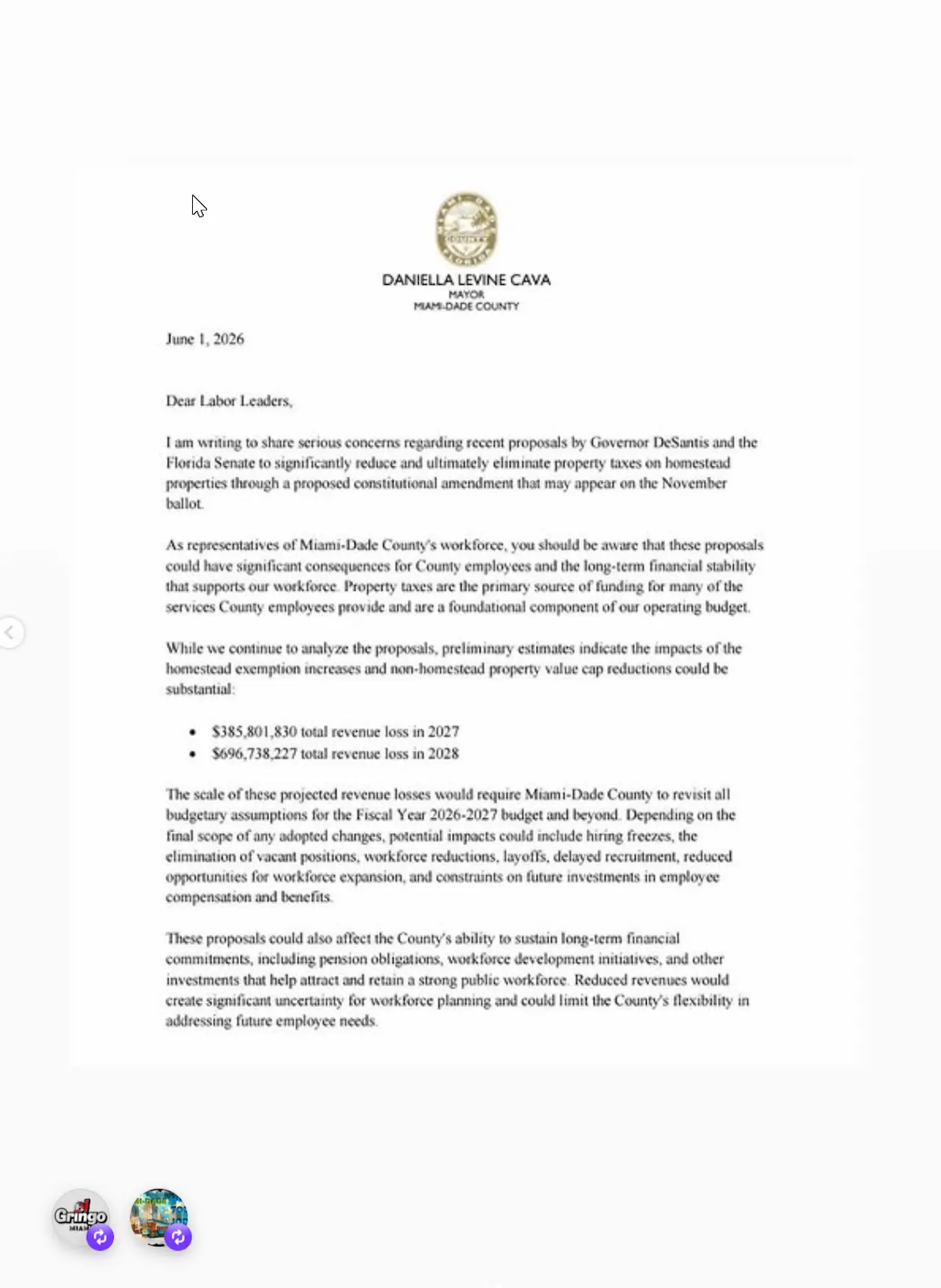

Ninth, direct letter to county labor leaders. On June 1, 2026 – the opening day of the special session in Tallahassee – Major Daniella Levine Cava sent a formal letter to labor leaders representing Miami-Dade County employees, warning of the potential fiscal and labor consequences of proposals by Governor Ron DeSantis and the Florida Senate to reduce and eventually eliminate property taxes on homestead properties.

The letter documents tax loss estimates that differ from the figures published in last month’s Miami Herald op-ed: $385,801,830 in total revenue loss for 2027 and $696,738,227 for 2028. Combined, the two figures total $1,082,540,057 over two years, compared to the cumulative $697 million cited in the May op-ed.

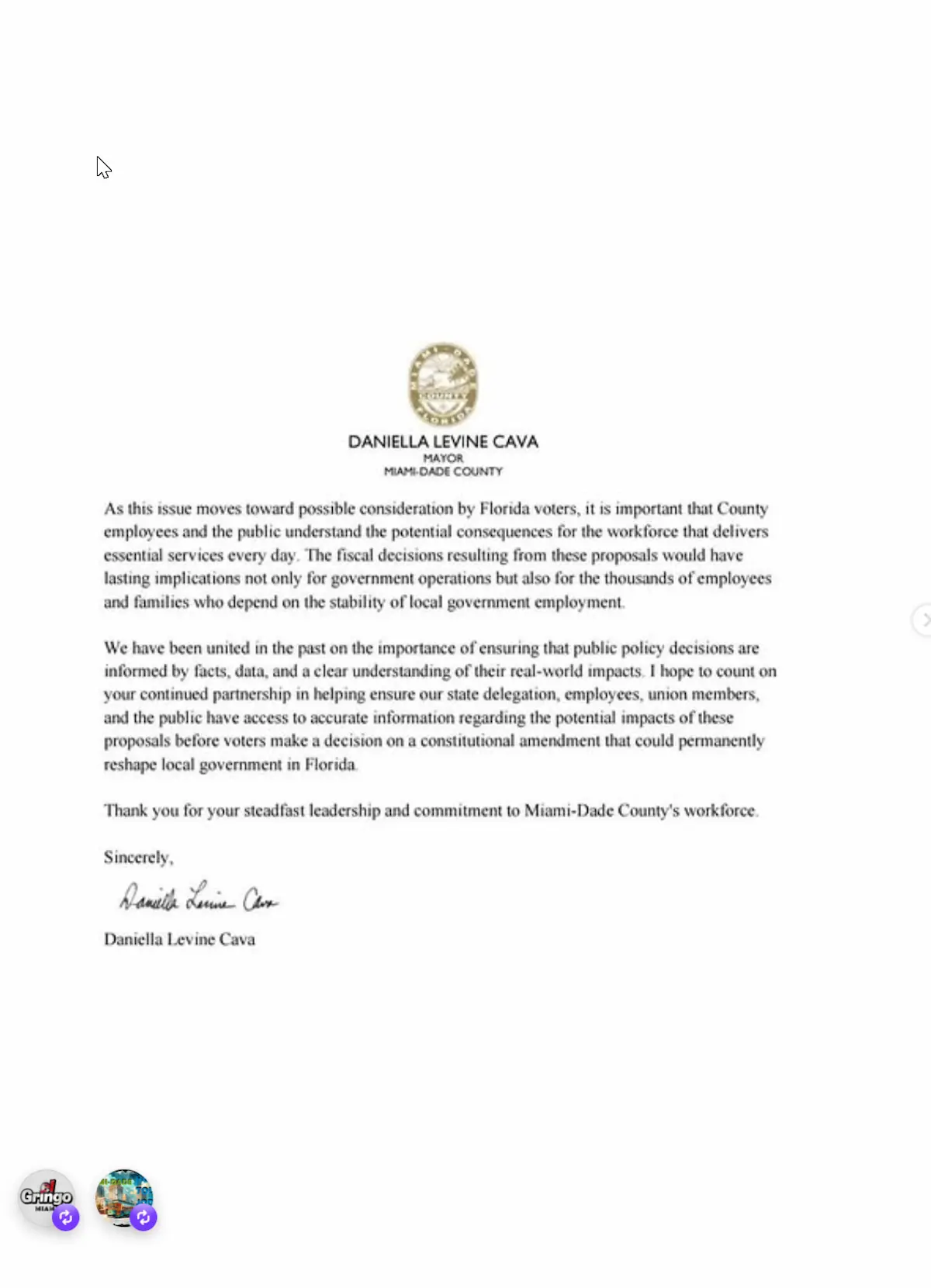

The letter also warns that, depending on the final scope of the adopted changes, impacts could include hiring freezes, elimination of vacant positions, staff reductions, layoffs, recruitment delays, reduced opportunities for workforce expansion, and future restrictions on investments in compensation and benefits for county employees.

In closing, Cava called on labor leaders to continue to collaborate to ensure that the state delegation, employees, union members and the public have access to accurate information about potential impacts before voters decide on a constitutional amendment that, according to the letter, could permanently reshape local government in Florida.

The numbers: between $340 and $977 million at stake in Miami-Dade

The impact figures for Miami-Dade documented vary by source and scenario considered. The following table consolidates the main estimates:

| Source | Figure | Period | Scenario |

|---|---|---|---|

| Mayor Cava (Policy Council BCC, 2 Feb 2026) | up to 900 million | total potential impact | more aggressive legislative text feb 2026 version |

| Major Cava (op-ed Miami Herald, May 2026) | 386 million in 2027 + 697 million in 2 years | ballot scenario november 2026 | version final amendment approved |

| Mayor Cava (union leaders letter, 1 Jun 2026) | $367.8M in 2027 / $609.7M in 2028 (annual; $977.5M combined) | FY 2027 + FY 2028 annual each year | final amended version; methodology differs from Herald op-ed. |

| Tomas Regalado, Property Appraiser MD | 925 million in 2 years | FY 2027-28 Miami-Dade specific | final amended version; methodology different from Cava |

| Florida Association of Counties | approximately 340 million annually | FY 2027-28 Miami-Dade specific | current amended version |

| Commissioner Danielle Cohen Higgins (BCC, 17 Mar 2026) | approximately 990 million | accumulated potential shortfall | maximum scenario |

| Carlos Migoya, Jackson Health (BCC, 3 Mar 2026) | 83 million per year | impact Jackson Health System | House version HJR 203 |

| Baseline FY 2026-27 (Axios Miami citing Cava) | 94 million deficit | state pre-impact operating deficit | unamended |

| Miami-Dade Property Appraiser’s Office (via WSVN 7News, Jun 2026) | $130M revenue county 2027 / $222M revenue county 2028 | Phase 1 (2027) + Phase 2 (2028) | county revenue only; average homeowner: nearly $1,700 in 2027 / nearly $2,800 in 2028 |

Statewide: $4.6 billion in lost revenue in 2027 and $8.4 billion in 2028. Broward would face $195 million in the first year and $333.8 million in the second. Hillsborough projects $478 million annually by 2028.

What about services

Mayor Cava listed at the March 17, 2026 Board of County Commissioners hearing the county services that would be affected:

“We have produced estimates of impacts. There’s been a recent Miami Herald article with estimates of impacts. Those impacts of course will affect not just our nonprofits. They will affect transit, animal services, road repair, parks, really every general fund component of our budget.”

In the same session, Cava warned that the effect could restrict even the future growth of essential services:

“We can’t say that even police and fire will be protected because it would be stopped at the current level. So that doesn’t allow for future growth and it only compounds the issue.”

The June 1 letter to union leaders adds the labor dimension to that impact: county employees could face position freezes, elimination of vacancies, staff reductions, layoffs, deferred recruitment and restrictions on compensation growth.

Chairman Anthony Rodriguez D10 warned in hearing of May 13, 2026 about the fiscal conflict with mental health:

“The governor and this legislature is talking about reducing or eliminating property taxes, we need to get comfortable with adding another 20 to 50 million dollars a year expense to this facility.”

If the amendment passes and local governments cannot absorb the loss of revenue through service cuts, alternatives documented by experts include: millage rate increases, new utility fees, increases in garbage collection fees, creation of special assessments and shifting the tax burden to the state level.

The cost of living in Miami-Dade and the unprecedented exodus in two decades

The property tax debate is not happening in the abstract: It is happening in South Florida’s most expensive county, where the cost of living pressures both homeowners and renters and has generated an exodus of residents that Census and IRS data measure as far back as 2022. The cost of living in Miami is 21 percent higher than the national average. Housing specifically is 58.7 percent more expensive. The average rent in Miami in June 2026 is $3,195 per month – 33 percent above the national average of $1,638.

A one-bedroom apartment averages $2,600 per month; a two-bedroom, $3,189. Only 11 percent of South Florida renter households can afford the mortgage payment on a single-family home at the median market rate.

The result is measurable: between 2023 and 2024, approximately 67,000 residents left Miami-Dade for other parts of Florida or the United States – the highest number of domestic departures in the last twenty years, according to the Census Bureau. Between July 2024 and July 2025, the outflow accelerated: more than 72,000 people left, and the county recorded a net decline of 10,115 residents, making it the third highest county in the nation to lose population during that period, behind only Pinellas County in Florida and Los Angeles County in California.

The domestic outflow has been partially offset by international immigration: between 2023 and 2024, about 124,000 people came to the county from abroad. But in 2026, that offsetting flow has begun to weaken: an April 6, 2026 Axios Miami analysis documents that the slowdown in international immigration is reducing the demographic buffer that Miami-Dade has relied on to maintain its population size in the face of domestic exodus.

This context introduces a paradox into the property tax debate. For those who leave, the elimination of the property tax comes too late: they have already left because they cannot afford the rent, not the property tax – because 89 percent of households that cannot afford to buy are not homestead owners either, and the amendment does not directly benefit them. For homeowners who stay and have homestead, the benefit is real and calculable: up to $2,800 per year less in taxes.

The law already in force: what CS/SB 4-F changes before the vote

The special session legislative package has two layers: constitutional amendment CS/HJR 1F, which goes on the November ballot and requires 60 percent of the voters, and implementation bill CS/SB 4-F, which became law on June 2, 2026 regardless of the November outcome. CS/SB 4-F changes Florida’s local government fiscal framework effective immediately and does not require voter ratification.

The central change in CS/SB 4-F is in section 200.065, Florida Statutes: the method for calculating the maximum millage rate cap. Under prior law, the maximum a county, municipality, or special district could charge without special approval was the rolled-back rate adjusted for the change in per capita income of Florida residents-a mechanism that allowed the cap to rise automatically with economic growth. CS/SB 4-F eliminates that adjustment: the cap is now the pure rolled-back rate.

To charge more than the rolled-back rate, local governments must follow one of two paths: up to 110 percent of the rolled-back rate, by a two-thirds vote of the governing body; above 110 percent, by unanimous vote, three-fourths vote if the body has nine or more members, or referendum.

CS/SB 4-F also reenacts sections 218.12, 218.125 and 218.136, Florida Statutes, which establish state compensation mechanisms for fiscally constrained counties. This mechanism is the legislative response to the concern expressed by Senator Hooper during debate: that the proposal, favorable to large urban counties, could be devastating to the state’s 31 poor counties.

What CS/SB 4-F does not include is equally significant. The implementing legislation contains no timetable, no formula, and no mechanism for the total elimination of the property tax homestead. Constitutional amendment CS/HJR 1F – if approved by voters in November – would mandate the Legislature to “design a path toward complete elimination” of the tax by general law. But it does not set when that law must be ready, or what it must minimally contain, or what happens if the Legislature fails to act.

What the amendment guarantees and what it does not: reading the rolled-up constitutional text.

The ballot proposition’s title is SAVE OUR HOMES FROM EXCESSIVE PROPERTY TAXES and the official summary says it “requires, through general law, a schedule for full elimination.” That difference between the title and the legal text contains the central tension that voters must assess before November. A reading of the rolled text of CS/HJR 1F – the 20 pages of the final document signed by both chambers – reveals precisely what is constitutionally guaranteed and what is subject to future decisions by the Legislature.

What the constitutional text directly guarantees if approved by the voters: as of January 1, 2027, the homestead exemption for all non-school levies rises from $50,000 to $150,000. Effective January 1, 2028, it goes up to $250,000. That figure is adjusted for inflation (CPI) beginning January 1, 2029.

The annual assessed value increase limit for non-homestead residential properties of nine units or less decreases from 10 percent to 5 percent, effective January 1, 2027. For commercial properties and other real estate not subject to the limitations of subsections (a) through (d), the same adjustment applies. The text also guarantees the new Section 9(2) use restriction – the seven categories – as permanent constitutional architecture.

What the text does not guarantee: the school levy remains at $25,000 exemption, unchanged. The Miami-Dade school district levy represents approximately 6.198 mills of the roughly 18-19 total mills paid by a homeowner in the unincorporated area-a significant portion of the annual bill that the amendment does not touch. For a home with an assessed value of $350,000 in 2028, the taxpayer will still pay the school levy on $325,000 ($350,000 minus the $25,000 school exemption), exactly the same as today.

The promise of “full elimination” is not a constitutional mandate with its own timetable. The text states that the Legislature “shall provide by general law a schedule for full elimination”. That obligation is directed to the Legislature, not written into the constitutional text with a date or mechanism for compliance. A future Legislature can fulfill that obligation by creating a plan with a 30- or 50-year horizon without violating the text of the amendment. There is no provision in the constitutional text or in CS/SB 4-F that establishes what happens if the Legislature fails to act, or within what time frame it must act.

The new residents clause takes immediate and visible effect. Anyone who establishes residency in Florida on or after January 1, 2027 – and who has not maintained permanent residency in the state as of December 31, 2026 – receives only a $50,000 exemption for five years. Only in the fifth year of homestead ownership does it scale to the full $250,000 level. This penalizes recent buyers financially in a direct and measurable way.

Category (g) of Section 9(2) deserves special attention because it is the component that mitigates the apparent restriction of uses. Its text states that ad valorem taxes may be used to “fund the operations and administration of county officers and commissioners…and municipalities, and the expenditures approved by such county officers or county or municipal governing bodies, except those expenditures prohibited by general law.”

The “expenditures approved by…governing bodies, except those prohibited by general law” clause is broad enough for a local government to argue that most of its current operating spending-including cultural programs, grants to nonprofit organizations, and economic development-falls within it, as long as the general law does not expressly prohibit it. The terms of that dividing line will be defined in future litigation.

CS/SB 4-F, already in effect as of June 2, 2026 regardless of the November vote, instead has an immediate and precise effect: the rollback rate – the rate that would generate the same revenue as the previous year – becomes the statutory millage ceiling. Previously, that ceiling was calculated with an adjustment for per capita income growth. That adjustment disappears. To exceed the rollback rate, Miami-Dade now needs a 2/3 vote of the BCC (to go up to 110% of the rollback) or unanimity or referendum (to go higher). This law already applies to the FY 2026-27 budget process that the county is now preparing.

The electoral timetable and the legal risk towards November 3, 2026

The Save Our Homes from Excessive Property Taxes amendment will be on the November 3, 2026 general election ballot. Pursuant to Florida Constitution Article XI Section 5, it requires ratification by 60 percent of the voters. This threshold was raised from 50 percent by a constitutional amendment passed in 2006 and has historically blocked multiple popular amendments.

Unlike citizen initiatives, legislative amendments are not automatically reviewed by the Florida Supreme Court before reaching the ballot. Legal experts consulted by PolitiFact anticipate that the proposal will face court challenges given its economic scope. As of the close of this piece, no lawsuit had been filed.

If the amendment is ratified, the implementation schedule is: on January 1, 2027, the $150,000 exemption goes into effect; on January 1, 2028, it rises to $250,000; the non-homestead limit drops from 10 percent to 5 percent simultaneously; the total phase-out schedule remains to be designed by general law.

The question to be decided by voters on November 3, 2026

At stake on the ballot on November 3, 2026 is a dispute over who defines local government efficiency. For Governor DeSantis and proponents of the proposal, Florida’s local governments have grown their budgets fueled by a housing boom that artificially inflated their tax base, and the amendment forces them to become more efficient while restoring purchasing power to family homeowners.

For Major Cava and opposing local governments, the cost of utilities does not disappear when the revenue disappears: it is shifted to renters, businesses and non-homesteaded property owners, or the service is eliminated.

Jeff Brandes, the state’s former Republican Senator, offered from within the party the most concise summation of that tension: “This is a tax shift, not a tax cut.” The Florida Association of Counties reinforces the argument in its official statement:

“Eliminating property taxes does not eliminate the cost of infrastructure, emergency response, and other essential local services. Those costs do not disappear, they shift somewhere else, often onto businesses, renters, and working families.”

That is exactly the question Florida voters will answer on November 3, 2026: whether local governments have a revenue problem that requires protecting the source, or a spending problem that requires reducing it.

Sources consulted

Level 1 – Official sources

- Miami-Dade County BCC Regular Meeting transcript March 17, 2026 (Item 6A1). Verbatim Major Cava, Commissioner Lopez, Commissioner Higgins. Public broadcast available on file with Granicus Miami-Dade. Local transcript processed by NMD:

archives/legistar/transcripts/bcc/2026/Transcrip BCC meeting 03-17-2026.txt. - Miami-Dade County BCC Policy Council Meeting transcript February 2, 2026 (Verbatim Major Cava up to $900 million). Public broadcast on file Granicus Miami-Dade.

- Miami-Dade County BCC Regular Meeting transcript March 3, 2026 (Verbatim Carlos Migoya 83 million annually). Public broadcast on file Granicus Miami-Dade.

- 4. Miami-Dade County BCC Committee Whole transcript May 13, 2026 (Verbatim Chairman Rodriguez). Public broadcast on Granicus Miami-Dade archive.

- 5. Miami-Dade County BCC Intergovernmental and Economic Committee transcripts 4 February + 15 April + 13 May 2026. Public broadcasts in Granicus Miami-Dade archive.

- 6. Miami-Dade County BCC Budget Hearings transcripts 4 September 2025 + 18 September 2025. Public broadcasts on file Granicus Miami-Dade. Verbatim Mayor Cava 18 Sep 2025: “Making any millage cuts now when we have prepared a fair balanced budget despite unprecedented financial constraints would be fiscally irresponsible.” Constitutional returns recorded at hearing: Tax Collector $13.5M + Clerk/Comptroller $5.3M. See also Sources 46, 53, 54 and 55 for detailed verbatim from that same hearing.

- 7. Florida Constitution Article VII Sections 4, 6 and 9 + Article XI Section 5 + Article XII (new SCHEDULE section created by CS/HJR 1F).

- 8. CS/HJR 1F (2026F Legislature) – Save Our Homes from Excessive Property Taxes. ENROLLED version. Sponsor: Rep. Toby Overdorf (R-Palm City). Text enrolled read in full (20 pp, hjr1f-01-er). Local copy:

archives/cases/cas/cas-016-desantis-property-tax-2026/sources/01-primary/HJR1F-enrolled.pdf. - 9. CS/SJR 2-F (2026F Legislature). Sponsor: Sen. Bryan Avila (R-Hialeah). CS/SB 4-F (state implementing legislation, also sponsor Avila): text enrolled read in full (9 pp, 20264Fer). Local copy:

files/casos/cas-016-desantis-property-tax-2026/sources/01-primary/SB4F-enrolled.pdf. - 10. Senate of Florida – Senator Bryan Avila (sponsor SJR 2-F + SB 4-F).

- 11. Executive Office of the Governor Florida – special session announcement and SaveOurHomes.